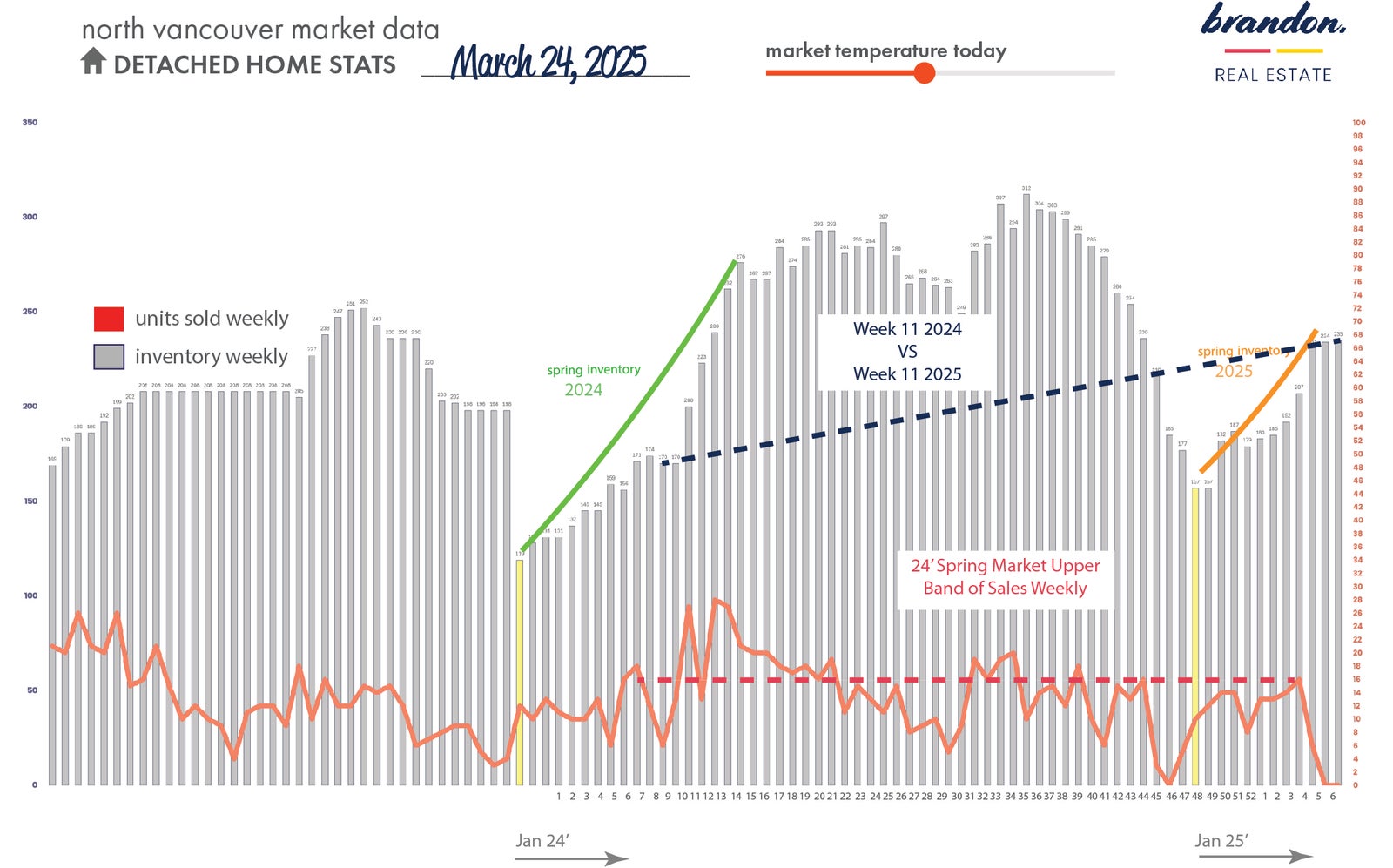

Detached Homes (North Van)

As of Monday, March 24thThe theme? "Few good homes, priced well.

This suggests we might see a major surge in listings over the next few weeks—potentially hitting Summer 2024 inventory levels sooner than expected.

- "Overpriced homes sit.

- Turnkey homes (minimal to no renos) are scarce.

- The $1.8M–$2.2M price range is the most active.

This suggests we might see a major surge in listings over the next few weeks—potentially hitting Summer 2024 inventory levels sooner than expected.

Sales: Holding steady (Red Line)

While general reports claim sales are down, the data suggests North Vancouver remains fairly level for this time of year. If last year’s pattern repeats, we could see a surge of activity in early April before inventory peaks and potential summer sales slow down.

While general reports claim sales are down, the data suggests North Vancouver remains fairly level for this time of year. If last year’s pattern repeats, we could see a surge of activity in early April before inventory peaks and potential summer sales slow down.

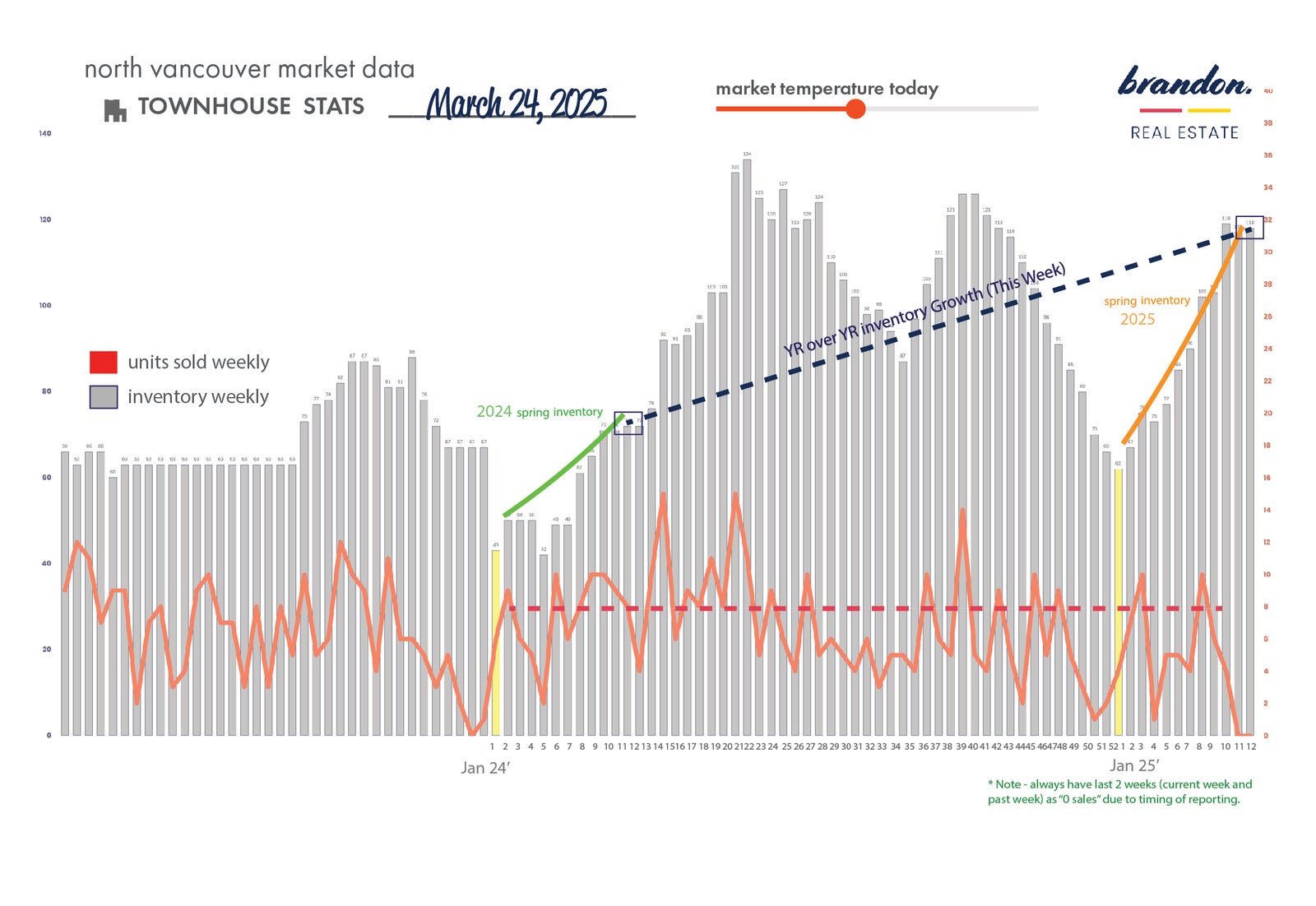

TOWNHOUSE (NORTH VAN)

Inventory: Up 26% year-over-year (Blue Line/Bar)

- Nearly half (48%) of available townhouses were built in 2020 or later.

- Are we witnessing a major demographic shift? (COVID-era babies now 5 years old = families needing backyards).

- Or are homeowners struggling with rate renewals after holding onto ultra-low mortgage rates for years?

Sales: Surprisingly strong (Red Line)

Despite rising inventory, demand is booming for $1.3M–$1.4M, 2-3 bedroom townhomes. These are moving fast, often in multiple offers—a clear sign of what buyers are looking for.

Despite rising inventory, demand is booming for $1.3M–$1.4M, 2-3 bedroom townhomes. These are moving fast, often in multiple offers—a clear sign of what buyers are looking for.

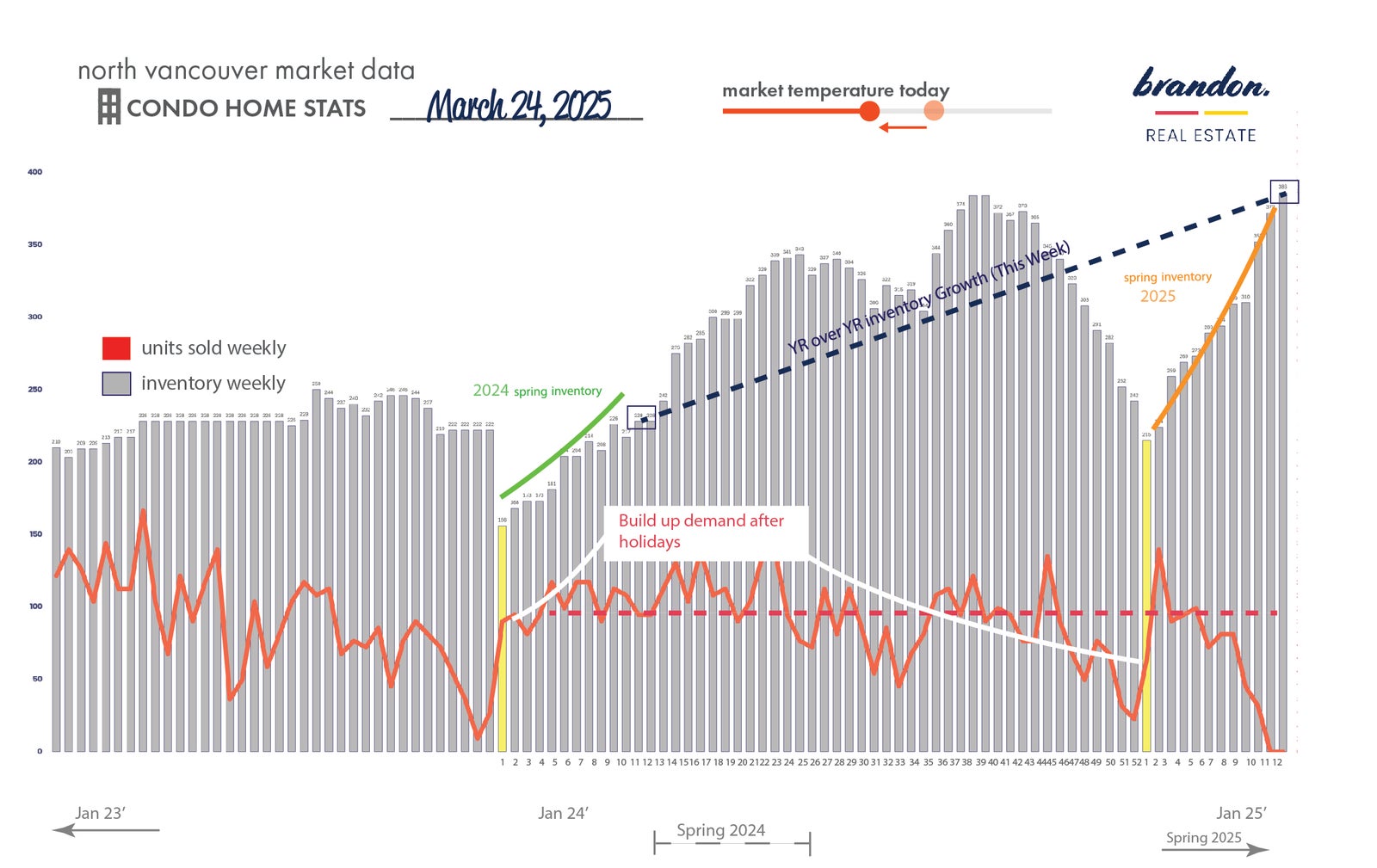

CONDO (North Van)

Inventory: Up 66% year-over-year (Blue Line/Bar)

Let that sink in—66% more inventory than before Spring Break last year.

Let that sink in—66% more inventory than before Spring Break last year.

- This just surpassed a 5-year inventory record (excluding early COVID, when condo listings hit 500 units before demand bounced back).

- 35% of available inventory consists of newer units (built 2020+).

- Are we seeing the same shift as in townhouses? Investors/homeowners adjusting to higher carrying costs?

Pricing Trends:

- Newer wood-frame condos are hitting $1,200/sq ft! 🤯

- Unique 1- and 2-bedroom units with views are still selling fast, often in multiple offers.

Sales: Turning a corner - While a touch slower than pre-summer 2024, buyer behavior suggests many are waiting on the sidelines—watching inventory levels and interest rates.

Market Outlook:

With all signs pointing to pent-up demand, we could see a rush of activity once buyers decide to move. Spring Market 2025 looks busy. While a touch slower than pre-summer 2024, buyer behavior suggests many are waiting on the sidelines—watching inventory levels and interest rates.

Market Outlook:

With all signs pointing to pent-up demand, we could see a rush of activity once buyers decide to move. Spring Market 2025 looks busy. While a touch slower than pre-summer 2024, buyer behavior suggests many are waiting on the sidelines—watching inventory levels and interest rates.